“We have a flash recession caused by a natural disaster. Normally natural disasters are regional. This natural disaster was not only countrywide but worldwide,” Don Ake, the FTR Intelligence vice president for commercial vehicles, said during a recent FTR Engage virtual session on commercial vehicle supply.

Despite the second wave of COVID-19 infections in the Sun Belt this summer, the U.S. economy “kept growing, kept moving, kept pushing right on through that second wave,” Ake said. Last week, Bob Costello, the American Trucking Associations’ chief economist declared the pandemic recession over and noted that trucking was not hurt the same way as other industries, unlike past recessions.

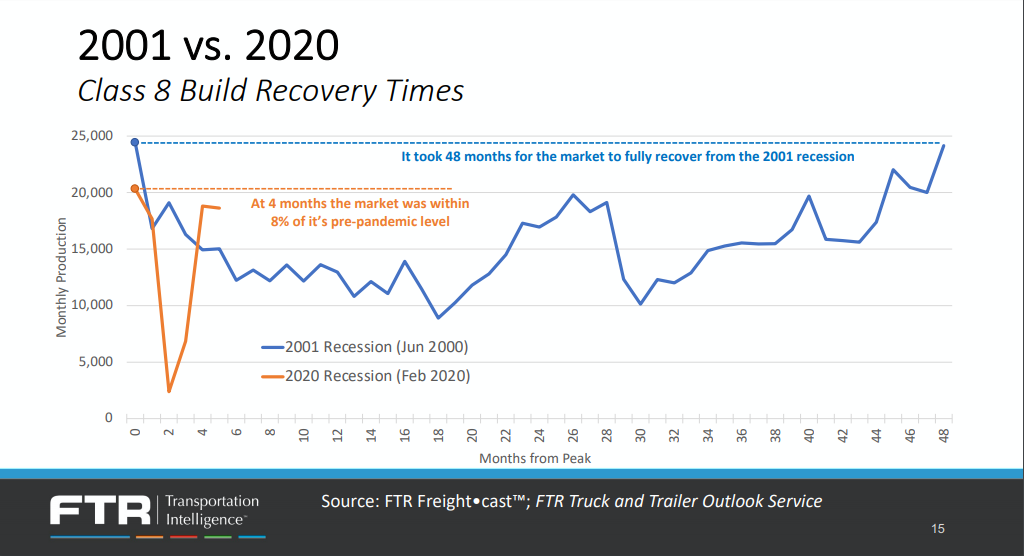

Class 8 vehicle sales are a leading economic indicator, Ake noted. And while there are not many economic periods to compare the coronavirus recession to, Ake pointed to the 2001 recession as a measuring stick. Eight months before that recession began, Class 8 sales started to drop in July 2000. “Even though it was considered a mild recession, it took 48 months for the market to recover back to the level before the slide began,” Ake said of the first recession of the 21st Century.

Fast-forward to the pandemic recession that pumped the brakes on the expanding U.S. economy in March: Just four months into the recession (based on the latest data available) and Class 8 builds were already within 8% of the pre-pandemic level. It took about 45 months to get that close to pre-recession levels after the 2001 recession.

With the Mexico market coming back online this summer, Ake expects the Class 8 build level to inch even closer to February numbers. “So we have a chance to get it much earlier,” he said in late September of a Class 8 recession rebound.

Preliminary Class 8 net orders surged in September, FTR reported on Oct. 2, hitting 32,000 units — the most since October 2018. September order activity is up 55% compared to August and 160% compared to September 2019. The big September has Class 8 net orders nearing 200,000 over the past 12 months.

During the FTR Engage session last month, Ake said he expects Class 8 orders to stay in the 20,000 to 30,000 range through the fourth quarter — baring any unexpected economic turmoil.

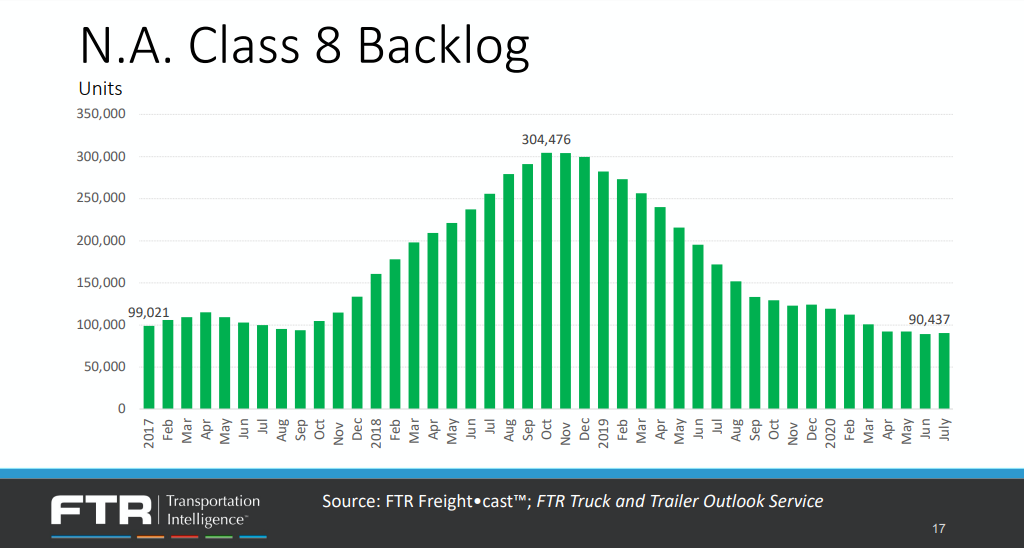

As of July, Class 8 backlog orders are also down to their lowest number since the start of 2017. At 90,437, that is well below the record back-order peak of more than 300,000 in October 2018. “So this is not a bad place to launch into 2021,” Ake said. “It’s not great … but not a horrible place to start.”

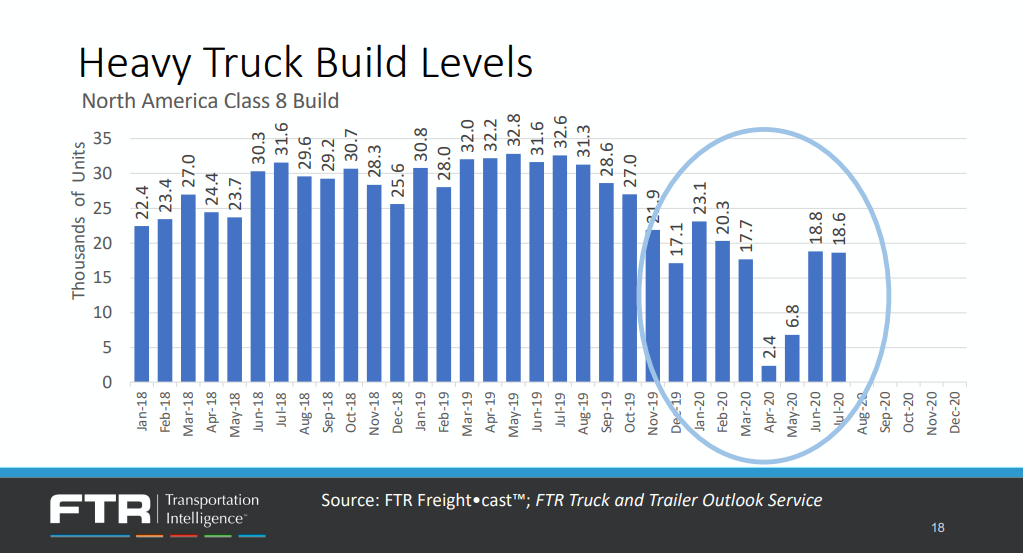

After the early pandemic days of uncertainty, when OEMs shut down production, heavy-truck build levels plummeted. But production has recovered, Ake noted. “There was a lot of uncertainty. We didn’t know how long it would take to climb back,” he said. “Fortunately, we’ve had some decent production in June and July, and the numbers are probably going to be higher in August because the Mexico market is recovering.”

The pent-up market demand that grew during the shutdown has helped spur the late-summer sales, Ake noted. “Trucks that would have normally been ordered then, are being ordered now since much of the risk has passed,” he said. “The order volume is very close to August’s trailer orders. Therefore, it appears the fleets took care of their trailer needs first and then caught up on the truck side in September.”

Orders for 2021 deliveries are expected to begin in October, giving the industry solid momentum as the year wraps up.

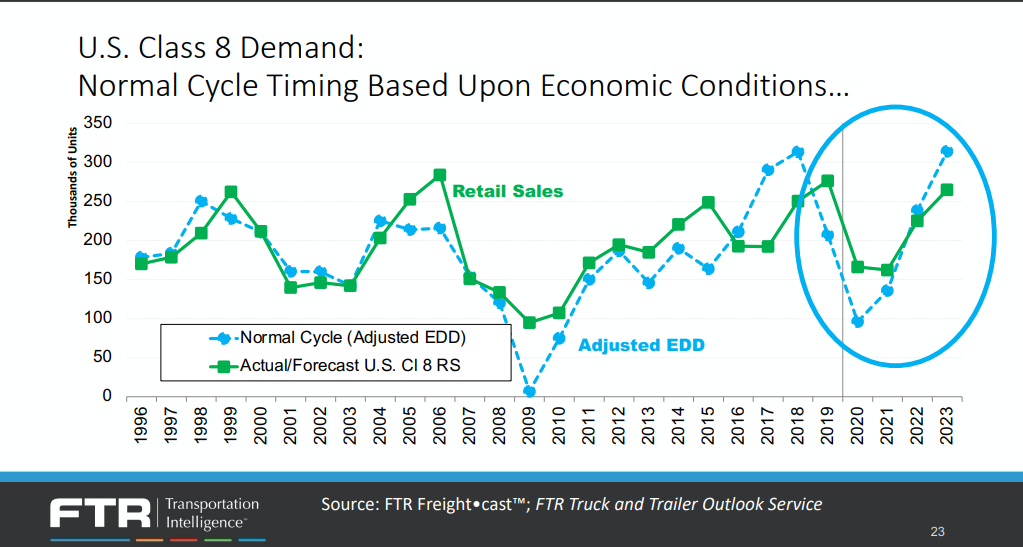

“As the market starts to recover, good things should happen,” Ake predicts. “We’re looking for a banner year in 2023 — looking for stuff to go higher than the 2018-19 cycle. Remember, the OEMs have added some capacity. So we think we can hit that number and there won’t be much capacity constraint — although you don’t know the market share between the OEMs.”

This article was originally published by American Trucker.